3.3 Lesson Three: Agile and robust economic policy Akoranga Tuatoru: He kaupapa here ōhanga urutau, pakari hoki

Lesson Three: Agile and robust economic policy

Akoranga Tuatoru: He kaupapa here ōhanga urutau, pakari hoki

L3.1 Lesson Three in brief

Akoranga Tuatoru – He Kōrero poto

A strong economy helped New Zealand respond to the COVID-19 pandemic. New Zealand's economic policy decisions now and into the future will be important for determining the country's ability to mount a strong response to the next pandemic or other shock.

The imminent arrival of a potentially deadly pandemic will likely again require quick action on the part of government to limit its incursion and spread. There will again be uncertainty about the course and duration of a new pandemic, the nature and severity of the accompanying shock to the economy, the impact of the public health interventions available, and the extent and type of economic supports required.

Short-term or easily reversible economic policy measures should be used to address immediate effects and buy time to gather more information, especially about the type, size and duration of the shock to the economy.

Not all decisions need be taken swiftly. Those made at speed should be reviewed as circumstances change and strategies adapt. Ongoing monitoring is needed to check that the chosen options are achieving their intended purpose, and whether significantly better options have become available, or previously unforeseen consequences have emerged.

The 'strategic function' recommended in Lesson One should prepare and maintain a short-form guide for decision-makers facing a pandemic or similar emergency.

We learned that macroeconomic forecasts were unreliable during the pandemic. Decision-makers should treat them with caution, and consider a range of plausible scenarios or possible paths the economy could follow.

The government's lead economic advisor, the Treasury, and the independent Reserve Bank, should clarify the roles of fiscal and monetary policies in the event of a large economic shock of uncertain nature and duration. This would assist in responding to the next pandemic, reducing the potential for unaligned economic policy responses.

If fiscal stimulus is considered necessary in a future pandemic, measures should be timely, temporary and targeted. Short-term supports that automatically adjust as circumstances change are preferable, and infrastructure maintenance and renewal should be considered ahead of new investment. The Treasury and the New Zealand Infrastructure Commission should investigate the feasibility of an infrastructure maintenance priorities programme.

Quantitative easing and other unconventional monetary policies used during the pandemic had significant costs. The Government should review the sections of the Public Finance Act 1989 that deal with giving Crown guarantees and indemnities. The Act should specify more robust and transparent processes for giving large guarantees and indemnities.

Additionally, the Treasury and the Reserve Bank should initiate a research programme to analyse the costs and benefits of unconventional monetary policies used in New Zealand and other countries during the pandemic. This should be done before such policies are used in future.

The Treasury, in conjunction with relevant agencies, should develop policy options for financial assistance schemes during a pandemic.

We learned that economic circumstances changed quickly during the pandemic. Stats NZ, in consultation with the Treasury and the Reserve Bank, should investigate the costs and benefits of more frequent releases of a wide range of macroeconomic indicators.

New Zealand, like many other countries impacted by COVID-19, is in a weaker position to weather the next large economic shock than it was at the start of the COVID-19 pandemic. There is a pressing need to reduce public debt to provide a buffer for future pandemics or other economic shocks. The best approach to reducing debt involves economic growth driven by productivity improvements, accompanied by disciplined fiscal management. The Treasury should publish a regular report on financial resilience, and this should guide the objectives stated in the Government's annual Fiscal Strategy reports.

L3.2 About this lesson | Mō tēnei akoranga

The pandemic, and the public health measures needed to contain it, had substantial economy-wide effects. In this Lesson we look at the economic situation during the pandemic and the economic policies adopted. This will assist in drawing lessons for economic policy for future pandemics.

Part 2 of this report addresses whether key decisions were sufficiently informed about possible effects on inflation, debt and economic activity. However, decision-by-decision assessments need further context to properly understand the full range of economic consequences of multiple decisions over the period, including consequences that were unforeseen at the time.

Given the dynamics of economic adjustment to shocks such as pandemics, and the lags between policy response and effect, we need to consider the whole pandemic period for context. Decisions made in 2020 had consequences during and after the period specified in our Terms of Reference. Economic policies during the period will have been in response to earlier developments, and some of the effects of economic policy decisions made between February 2021 and October 2022 will not have become apparent until later.

By looking at the entire pandemic period, and with the benefit of hindsight, we can see the effect of the overall approach to economic policy. Our intention in this Lesson is not to evaluate specific policy decisions but rather to identify and characterise policy approaches that might help New Zealand avoid unforeseen

In writing this lesson we have brought together evidence from a range of sources.

We have examined the advice officials gave about economic conditions and the sustainability of the economic supports provided to businesses and workers as part of the key lockdown decisions in the period under inquiry (see chapter 2.4).

We have heard from people whose businesses and livelihoods were affected during the pandemic, particularly during the Auckland lockdown commencing in August 2021.1066

We draw on the economic analysis in the Phase One report, and the wider economic literature. We have an extra year of data and analysis over that available to Phase One, allowing economists and others more time to reflect.

We also draw on publicly available data and our own research, especially comparisons between New Zealand's pandemic response and its economic consequences, and those of other jurisdictions. These too, can provide lessons for New Zealand for a future pandemic.1067

In addition, we talked with senior officials from that time, independent economists and academics,1068 and former Ministers.1069 We have also referred to recent work by the New Zealand Treasury1070 and the Reserve Bank of New Zealand,1071 looking back on fiscal and monetary policy during the COVID-19 response.

L3.3 What we learned from New Zealand's COVID-19 experience

Ngā mea i akona mai i te wheako o Aotearoa ki te KOWHEORI-1

The Government responded quickly to COVID-19 by closing the external border and restricting the movement of people to avoid or limit incursion and spread of the virus. At the same time, the Government launched an initial package of economic supports for firms and households.

These quick actions by the Government were taken at a time of deep uncertainty about the likely course and duration of the pandemic, the nature and severity of the shock to the economy, the impact of public health interventions and the extent of economic supports required.

Governments have a range of economic policy tools they can use to manage the economy, including dealing with adverse economic shocks – significant, disruptive events that have impacted on the economy (Box 1).

| Box 1: Economic policy tools for dealing with shocks | ||

|---|---|---|

|

Fiscal policy and monetary policy are the two broad sets of macroeconomic tools that can be used to mitigate the downsides of an adverse shock to the economy. Fiscal policyGovernments can directly absorb the effects of a shock on households and firms. For example, government can buy out owners of properties severely damaged in an earthquake and subsidise the wages bill of firms experiencing reduced revenue (helping them retain and pay their staff), as occurred during the pandemic. Government responses of this nature effectively transfer a part of the shock onto the government's books – in effect to (future) taxpayers. Such transfers mitigate a contraction in private spending and demand for goods and services resulting from the shock and thus lessen adverse effects on the wider economy. Governments can also bolster demand for goods and services in the economy by:

Unless paid for by current taxpayers, all the above contribute to fiscal stimulus in the economy. Monetary policyMonetary policy seeks to influence interest rates faced by households and firms. In New Zealand, monetary policy is managed independently by the Reserve Bank, rather than directly by the Government. Interest rates (on money borrowed in New Zealand dollars) are anchored by the overnight or 'official' cash rate (OCR) set by the Monetary Policy Committee of the Reserve Bank.1072 Higher interest rates dampen household and business consumption, and discourage investment in expanded supply, whereas lower interest rates stimulate both consumption and investment. There are significant lags in economic responses to OCR changes. For example, interest rates with longer fixed terms take a while to adjust, and prices for labour, goods and services can be 'sticky'. Central banks can undertake so-called 'unconventional' monetary policies. One example is the use of quantitative easing to inject liquidity into the banking system (as banks in some countries did during the Global Financial Crisis). Quantitative easing can serve two purposes.

The Large-Scale Asset Purchase programme was New Zealand's quantitative easing response during the pandemic. It involved the purchase of large quantities of financial market assets, aiming to lower longer-term (fixed rate) borrowing costs for households and firms. When official interest rates are at or close to zero, central banks have further unconventional monetary policy tools that can provide additional stimulus.

|

||

How to apply monetary and fiscal policy tools is well known once there is a good understanding of the type, size and duration of a shock. However, their application is challenging when there is deep uncertainty about these factors.

L3.3.1 COVID-19 created a large but unusual type of economic shock

I hua ake i te KOWHEORI-19 tētahi rū ōhanga nui, rerekē hoki

Aotearoa New Zealand has experienced numerous adverse economic shocks during its history. The economy suffered from the fallout from overseas financial crises such as the Asian Financial Crisis in 1998 and the Global Financial Crisis in 2008-09. Also, natural disasters have damaged New Zealand's productive assets, such as the Canterbury (2010, 2011) and Kaikōura (2016) earthquakes, and the North Island weather events of 2023. Going back further, the 1966 wool price shock, the 1970s oil price shocks, and the United Kingdom's 1973 entry into the European Common Market all had significant, although different, impacts on the New Zealand economy.

The COVID-19 pandemic was a substantial shock to the New Zealand economy. The economy, as measured by real GDP (Gross Domestic Product)1073 shrank by 11.4 percent between December 2019 and June 2020, then rebounded to higher than its prior level.1074 It dipped again by 4.2 percent between June and September 2021. However, over the calendar years 2020 and 2021, the economy grew by a total of 4.1 percent.1075 By contrast, during the Global Financial Crisis, the economy shrank by 2.5 percent,1076 and did not consistently regain its previous high until 2011.

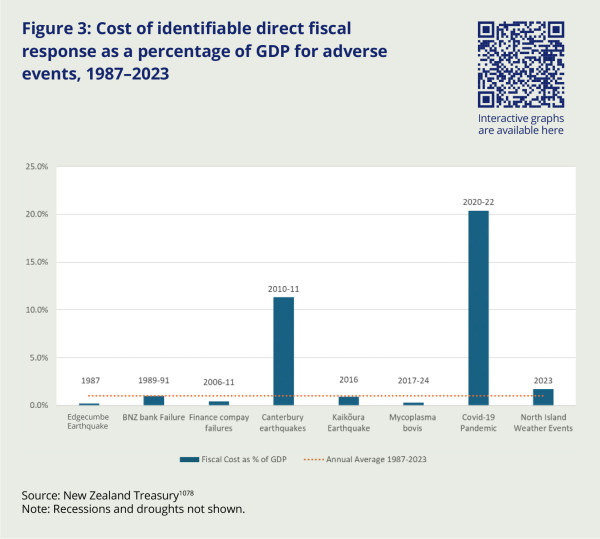

By one measure, the COVID-19 pandemic was the costliest event in terms of fiscal support in New Zealand in the past 40 years.1077 At 20.4 percent of annual GDP, the identifiable direct fiscal response to the pandemic was almost twice that of the response to the Canterbury earthquakes, and 12 times that of the 2023 North Island weather events. The earthquakes and weather events were geographically localised, whereas the pandemic was a national (and international) phenomenon. Figure 3 shows the direct fiscal costs of several significant adverse events in New Zealand over the past four decades.

Figure 3: Cost of identifiable direct fiscal response as a percentage of GDP for adverse events, 1987–2023

L3.3.2 Understanding the type of economic shock caused by a pandemic, and why that matters

Te mārama ki te momo rū ōhanga ka hua mai i te mate urutā, me te take nui o tēnei māramatanga

At the broadest level, economists distinguish between supply and demand shocks. Adverse supply shocks are those that decrease the quantity of goods and services produced and raise prices. For example, a 'dry year' electricity shortage can cause a spike in electricity prices, and production cutbacks in industries where electricity is a major input. Adverse demand shocks are those that negatively impact spending in the economy. For example, a sharp rise in overseas tariffs will reduce the demand for New Zealand goods and services and thus New Zealanders' incomes. Also, regardless of the type of shock, economic confidence can be affected resulting in greater precautionary savings and reduced consumption and investment by firms and households.1079

At the outset of the pandemic, there was deep uncertainty about the direct and indirect effects on the global and national economies. Economists foresaw the likely curtailment of production, accompanying loss of income, and a major impact on business and investment confidence and economy-wide demand for goods and services. The clear weight of economic sentiment was negative, with initial projections of a global recession.

It is apparent that many initial assessments of the situation were shaped by the experience of the world economic shock in 2007-2008 – the Global Financial Crisis.1080 This was a demand shock, stemming from severe contraction in the availability of money and credit. In that circumstance, governments and central banks took unprecedented steps to prop up financial systems and arrest what was an emerging possibility of a spiralling collapse in financial and economic confidence.

There were parallels between the initial economic response to the pandemic and the Global Financial Crisis. Governments and central banks moved to prop up demand, using fiscal and monetary policies to provide economic stimulus. In New Zealand, those policies included subsidising the wage costs of firms experiencing reduced revenue (helping them retain their staff), cutting the OCR to 0.25 percent and introducing quantitative easing. The initial imperative was to avoid a collapse of confidence and economy-wide demand for goods and services.

There were, however, some cautionary voices. In March 2020 Kenneth Rogoff, Professor of Economics and Public Policy at Harvard University, wrote that COVID-19 and the response to it would significantly affect economic production – that is, the supply side of the economy.1081 As events unfolded, and the effects of lockdowns and resulting disruptions to supply chains became more evident, recognition of the 'supply shock' nature of the pandemic came more to the fore (Table 7).

Table 7: Timeline for the shift toward a supply-shock interpretation (selected papers)

| Date | Authors | What it showed |

|---|---|---|

| March 2020 | Kenneth Rogoff | Warned that COVID-19 would resemble a supply-side shock, not a standard demand-side recession. |

| March 2020 | Kenneth Rogoff | Warned that COVID-19 would resemble a supply-side shock, not a standard demand-side recession. |

| April 2020 (published August 2020) | R Maria del Rio-Chanona et al.1082 | Sector-level modelling showed large supply-side constraints (labour availability, shutdowns) dominating effects. |

| April 2020 | Guerrieri, Lorenzoni, Straub & Werning1083 | Showed how a supply shock can trigger a demand shortfall, but emphasised initial disturbance is supply-side. |

| June 2020 | Duarte, Faria-e-Castro & Brinca1084 | Decomposed United States data and found supply shocks drove most of the fall in hours worked between March and April 2020. |

| July 2020 | Jonathan Haskel1085 | Concluded that COVID-19 is best described as a supply shock – a change to the extent to which the economy can provide goods and services. |

| January 2021 | European Central Bank1086 | Concluded the COVID-19 shock was both a demand and supply shock, but highlighted persistent supply constraints, especially labour and production bottlenecks. |

Source: NZ Royal Commission of Inquiry into COVID-19 Lessons Learned: Phase Two analysis

The studies in Table 7 all use consistent macroeconomic frameworks that apply to New Zealand and other countries equally. While domestic policy choices were different, the type of economic shock is the same across all countries.

The importance of this shift in thinking is that the policies for mitigating a supply shock differ markedly from those for a demand shock. If the event underlying an economic shock adversely affects production, then beyond responding to the immediate loss of business confidence, monetary and fiscal policy needs to adapt to take account of the curtailment of supply. Without that adaptation, there is a risk of monetary and fiscal stimulus leading to excess demand and upward pressure on prices, particularly for those goods and services where supply is constrained.

In New Zealand, by the second half of 2020, that risk had eventuated, even if it was not fully appreciated at the time. By then the initial nationwide lockdown had been lifted, and a degree of normalcy and economic confidence had been restored. Fears of economic collapse had dissipated and there were signs of economic adaptation to restrictions. For example, New Zealanders vacationed locally, partially substituting for the loss of inbound tourists, and there was labour redeployment, such as airline flight crew and travel agents finding new roles. Overall, the economy, firms and households exhibited a capacity to adjust and adapt, probably more than initially expected.

Nevertheless, the fiscal and monetary stimulus continued into 2021, as described in Section L3.3.5.

L3.3.3 Early advice emphasised timely, temporary and targeted economic policies

I whakanui te tohutohu tōmua i ngā kaupapa here ōhanga kia wā-tika, kia poto, kia ū ki te whāinga

We now turn to New Zealand's economic response to the pandemic. The Treasury's advice to the Minister of Finance on 21 February 2020 presented three scenarios. All were weighted toward needing fiscal stimulus to respond to a demand shock to the economy caused by the impending arrival of the pandemic.1087 Follow-up advice on 6 March 2020 focused on one of those scenarios.1088

Notwithstanding the initial advice, the Treasury and the Ministry of Business, Innovation and Employment emphasised that fiscal stimulus measures to address the economic consequences of the pandemic should be 'timely, temporary and targeted' (Box 2).1089 This advice balanced the need to act quickly with incomplete information against the risks of adopting difficult-to-reverse measures that might prove unsuitable (or no longer the best choice) should conditions change or more information became available.

| Box 2: Questions to ask of a proposed measure: will it be timely, temporary and targeted? | ||

|---|---|---|

|

||

The advice recognised that it is important to avoid locking in policies that create commitments that may not fit with changed circumstances. It is also important that early and rapid decisions are subject to review, ideally under less pressured conditions.

The early Treasury and Ministry of Business Innovation and Employment advice that the economic response to the arrival of COVID-19 should be timely, temporary and targeted was especially applicable in the highly uncertain circumstances the Government was facing in early 2020.

L3.3.4 Early decisions focused on income support and fiscal and monetary stimulus

I arotahi ngā whakatau tōmua ki te tautoko pūtea whiwhinga me ngā whakaohooho ā-tahua, ā-moni hoki

This section describes the economic policies implemented in 2020. These policies shaped and constrained the choices made between February 2021 and October 2022, the focus of our Terms of Reference.

In line with other countries, New Zealand's response to the pandemic involved both fiscal responses (such as supporting people's incomes and an increased public spending claim on resources) and monetary responses (such as lowering interest rates and providing liquidity support for the functioning of financial markets).1091

L3.3.4.1 Income support | Tautoko pūtea whiwhinga

The Wage Subsidy Scheme was the largest single economic policy measure adopted during the pandemic, costing $18.0 billion (Box 3).1092

| Box 3: The Wage Subsidy Scheme | ||

|---|---|---|

|

The Scheme subsidised employers whose revenue had dropped significantly (by 30 percent, later 40 percent) due to lockdown restrictions, encouraging them to retain their employees. The Scheme served public health, labour market and macroeconomic objectives:

|

||

The design of the Wage Subsidy Scheme was consistent with the timely, temporary and targeted criteria. It was timely in that money entered the economy quickly, it was targeted to employers facing a sizeable drop in revenue and was temporary in that it applied only while lockdowns restricted the ability to work (see chapter 2.4 for details).

L3.3.4.2 Fiscal stimulus | Whakaohooho ā-tahua

The Government introduced an initial $12.1 billion fiscal package in March 2020 'to support New Zealanders and their jobs from the global impact of COVID-19,' with a specified component 'for income support and boosting consumer spending.1094 The funding envelope grew quickly with the addition of the COVID 19 Response and Recovery Fund in April 2020 (see Box 4).

| Box 4: COVID-19 funding | ||

|---|---|---|

|

Faced with unexpected costs out of the normal budget cycle, the Government announced an initial response package to COVID-19 of $12.1 billion on 17 March 2020. In Budget 2020 (14 May) the Government established the COVID-19 Response and Recovery Fund to support New Zealand's response to and recovery from COVID-19. The Fund covered a wide range of activities and initiatives. Initiatives directly related to the pandemic included health system costs, the vaccination programme, business loan schemes, wage subsidies, and the managed isolation and quarantine system. However, around half of the total spending was not directly related to the pandemic, including infrastructure projects, and nature conservation and school lunch programmes.1095 Rather than being an actual sum of money ring-fenced by the Government for COVID-19 related purposes, the Response and Recovery Fund was a funding envelope for budget management purposes. It provided an indication of what the Government would be willing to spend, if necessary, to mitigate the impacts of COVID-19 on the health of New Zealanders and the economy.1096 The Response and Recovery Fund was formally closed as at Budget Day 19 May 2022; subsequently, remaining COVID-19 spending and future fiscal impacts were incorporated into the standard Budget and fiscal processes, though records of funding decisions were compiled up to 30 June 2022. The size of the fund at closure was $61.6 billion. Before any money in the Response and Recovery Fund was spent, it needed to be formally appropriated to a Vote.1097 $58.4 billion was allocated from the Fund. Adding this to the initial response package of around $12 billion gives a total allocation of $70.4 billion to more than 821 initiatives.1098 $70.4 billion is commonly cited as the fiscal Though the COVID-19 Response and Recovery Fund was formally closed in the 2021/22 fiscal year, many of these initiatives continued into subsequent years and were managed through standard fiscal processes. At the time of closure, some initiatives were forecast to have continued expenditure out to 2026. Not all money appropriated ended up being spent. A recent Treasury publication lists $66 billion as the fiscal cost of the response.1100 |

||

We have described the Wage Subsidy Scheme (see Box 3), the largest component of the COVID-19 Response and Recovery Fund. Another Fund initiative was the Shovel-Ready Programme, described in Box 5. It became the fourth-largest component of the COVID-19 Response and Recovery Fund.

| Box 5: The Shovel-Ready Programme | ||

|---|---|---|

|

The purpose of the Shovel-Ready Programme was to provide immediate economic stimulus, create and protect jobs, and accelerate infrastructure investment that was already planned or in late design stages but delayed by funding or consenting bottlenecks. The Government's announcement on 1 July 2020 said that the infrastructure investments would 'help kick-start the post-COVID rebuild by creating more than 20,000 jobs and unlocking more than $5 billion of projects up and down New Zealand'.1101 The COVID Response and Recovery Fund established in Budget 2020 had earmarked $3 billion for infrastructure projects.1102 Initial allocation decisions included $464 million for housing and urban development; $460 million for environmental projects; $670 million for community and social development projects; and $708 million for transport (cycleways, walkways, ports and roads). The announcement said the projects were in addition to the $12 billion New Zealand Upgrade Programme and existing Provincial Growth Fund investments. According to Finance Minister Grant Robertson, the Programme was 'about creating jobs as we recover and rebuild from the recession caused by the global COVID-19 pandemic. Because we went hard and early with our health response, we've been able to open up the economy quicker than other countries and get a head start on our recovery.'1103 |

||

As the announcement confirms, the Shovel-Ready Programme was on top of the previously announced New Zealand Upgrade Programme. The Government had announced the latter in January 2020, just before COVID-19 arrived in New Zealand. Together, these programmes represented $15 billion of direct government infrastructure investment.

The Shovel-Ready Programme was not targeted to costs arising from the pandemic. Also, shovel-ready projects are not by nature timely or temporary. Despite the name, they cannot be started immediately; they take time to ramp up, are difficult to stop, and typically run over many years. These constraints played out in 2021 and beyond.

In total, the COVID-19 Response and Recovery Fund encompassed more than 820 initiatives, totalling more than $60 billion. We have outlined two of the largest initiatives. One was by design timely, temporary and targeted, and the other was not. Spending initiatives that had longer-term consequences, but were not easily reversible, constrained the options available to decision-makers when the macroeconomic environment shifted in 2021.

L3.3.4.3 Monetary stimulus | Whakaohooho ā-moni

Monetary policy decisions are made by the Reserve Bank's Monetary Policy Committee (see Box 1). The Government sets the Committee's objectives via a remit. At the start of February 2021, the Committee's operational objectives were to 'keep future annual inflation between 1 and 3 percent over the medium term, with a focus on keeping future inflation near the 2 percent midpoint' and to 'support maximum sustainable employment'. A new remit came into force on 1 March 2021, adding a requirement for the Committee 'to assess the effect of its monetary policy decisions on the Government's policy to support more sustainable house prices.'1104

Particular decisions taken by the Monetary Policy Committee during the COVID-19 pandemic are outside the scope of this Inquiry. However, because monetary and fiscal policy interact, we describe the monetary policy response in general terms, including the evolution of that approach through the course of the pandemic.

On 16 March 2020 the Monetary Policy Committee lowered the Official Cash Rate (OCR) to 0.25 percent, committed to not changing the rate for 12 months, and launched a Large Scale Asset Purchase (LSAP) programme.1105 These measures were 'to provide economic stimulus' and 'keep interest rates … low.'1106 The LSAP would also support the functioning of the government bond market, which was experiencing high levels of uncertainty. In November 2020 the Monetary Policy Committee announced the Funding for Lending (FLP) programme, which provided low-cost financing to banks.1107

Table 8 sets out the Reserve Bank's description of the monetary tools it used.

Table 8: Monetary policy tools used during the COVID-19 pandemic

| Tool | Description | Date implemented |

|---|---|---|

| OCR | The OCR was lowered from 1.00% to 0.25%. | 16 March 2020 |

| Forward guidance | A commitment was made that the OCR would not change for at least 12 months from 16 March 2020. | 16 March 2020 |

| Large Scale Asset Purchase (LSAP) programme | The Reserve Bank undertook to purchase a significant amount of New Zealand government and Local Government Funding Agency bonds, in order to lower long-term interest rates. | 23 March 2020 ($30b limit) 7 April 2020 ($33b limit) 13 May 2020 ($60b limit) 12 August 2020 ($100b limit) |

| Funding for Lending programme (FLP) | The FLP is a low-cost funding facility for banks. It is equivalent in size to 6% of participants' loans. The facility lowers banks' funding costs directly, and also indirectly by reducing the cost of their other sources of funding. | 7 December 2020 |

Note: The limits on LSAP purchases were not reached. The Bank purchased around $53 billion of bonds in total.

The context for these decisions is important. Prior to the pandemic at the beginning of 2020, the OCR was at 1 percent, a level considered low. That left limited scope for the Monetary Policy Committee to lower the OCR further. The Monetary Policy Committee considered that 0.25 percent was the effective lower bound; that is, the point at which further cuts to the

OCR would be impractical or ineffective, primarily because of operational constraints and concerns about the transmission of negative interest rates through the banking system. Unable to lower the OCR further, the Monetary Policy Committee looked to unconventional monetary policies to provide stimulus beyond a 0.75 percent cut to the OCR, including forward guidance, and the Large Scale Asset Purchase and Funding for Lending programmes.

Central banks use forward guidance to make the future path of interest rates clear (for example, in New Zealand, the Monetary Policy Committee announced in March 2020 that the OCR would remain at 0.25 percent for the next 12 months). Forward guidance is a commitment to the market, but it comes at the cost of reducing the Committee's future options – options that are valuable should conditions change.

The Large Scale Asset Purchase programme had a short-term purpose of supporting the functioning of the bond market. As the programme continued and expanded, its purpose was to reduce longer-term bond yields by 'weight of money'.1108

Because the Bank was purchasing bonds when interest rates were at the effective lower bound, subsequent sales of bonds would more likely than not occur when interest rates were higher. In consequence, the Bank could expect to lose money on those sales. The programme would therefore incur financial losses.

The Reserve Bank applied to the Minister of Finance for an indemnity under the Public Finance Act 1989 against such losses. That indemnity (granted by the Minister of Finance in stages between March and August 2020) made the Crown directly liable for potential losses.1109 Losses from the Large Scale Asset Purchase programme turned out to be significant, with recent estimates putting them around $10.5 billion.1110

The programme was thus a monetary policy tool with large fiscal consequences, blurring the boundaries between monetary and fiscal policy. Further, the possible fiscal costs were not subject to the level of scrutiny as, for example, a budget bid with the same cost.

The Funding for Lending programme allowed eligible banks to borrow from the Reserve Bank at the OCR. Banks were thus less reliant on more expensive deposits and wholesale borrowing, lowering their overall funding costs. Banks could pass on the reductions to their customers through lower mortgage and business-lending rates. Access to the programme closed on 6 December 2022 and banks had to pay back the money borrowed on maturity. The final loans matured at the end of 2025.

Taken together, these monetary policies amounted to the provision of unprecedented levels of monetary support for the economy in 2020. Some of this support persisted into 2025.

L3.3.4.4 Both fiscal and monetary policies were highly stimulatory going into 2021

I tino kaha te whakaohooho a ngā kaupapa here ā-tahua, ā-moni hoki i te urunga atu ki te tau 2021

Throughout 2020, fiscal and monetary policies were aligned – both were highly stimulatory. Further, as described above, the design of some of these policies meant they would be difficult to unwind should circumstances change.

L3.3.5 The stimulus from 2020 decisions flowed into 2021

I kuhu tonu te whakaohooho i ahu mai i ngā whakatau o 2020 ki roto i te tau 2021

Between the end of the national lockdown in May 2020 and February 2021, New Zealanders faced few restrictions on domestic activities. While there had been several small COVID-19 outbreaks at the border, these had been quickly brought under control by contact tracing and isolation or by short-duration lockdowns. Vaccine rollouts were underway overseas and would soon start in New Zealand.

On the economic side, economic activity as measured by GDP had bounced back strongly after a sizeable dip in the second quarter of 2020.1111 Consumer price inflation remained low.1112 Businesses were generally holding up, except those dependent on international travel (such as tourism and international education).

There had been significant income replacement, notably through the Wage Subsidy Scheme. Together with the continuation of monetary and fiscal stimulus at a time of constraints on the ability to spend, the upshot was a build-up of household savings.1113

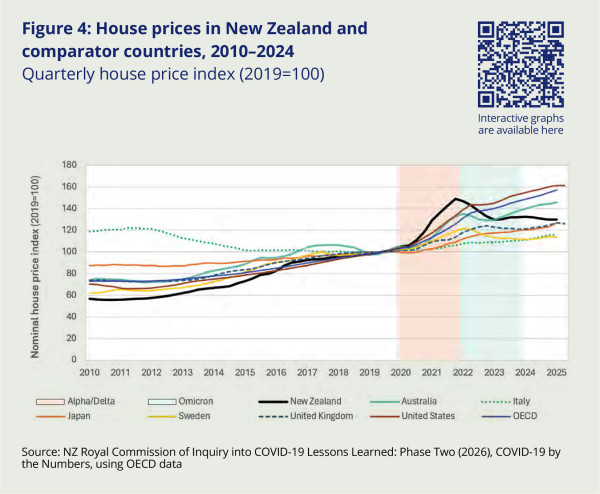

Some of this saving was simply deferred spending. However, some saving went towards asset purchases, pushing up asset prices. By late 2020, house prices – a long-standing issue for New Zealand1114 – had taken off. New Zealanders typically hold a large proportion of their wealth in housing: the low interest rates on offer at the time (below 3 percent for 5-year terms)1115 further encouraged households to invest in real estate. Relatedly, the experience of lockdowns and working from home increased the value of quality housing, and many households sought to upgrade.

House prices peaked in late 2021, during the Auckland lockdown, before partially retracting. House price inflation also occurred in comparable countries with similar monetary and fiscal stimulus policies1116, though the peak was more dramatic in New Zealand (as shown in Figure 4).1117

Figure 4: House prices in New Zealand and comparator countries, 2010–2024

Quarterly house price index (2019=100)

The surge in house prices stands in sharp contrast with earlier expectations that house prices would fall. The Reserve Bank projected in its May 2020 Monetary Policy Statement that house prices would fall by 9 percent by the end of 2020. Most economic commentators foresaw house prices falling by at least that much.

Looking back, the extent of the surge in house prices provides a reasonably clear indication that macroeconomic support – fiscal and monetary policy combined – was greater, and continued for longer, than was needed to maintain macroeconomic stability. This is consistent with a 2025 Reserve Bank assessment that, 'in hindsight earlier or faster tightening may have delivered better inflation outcomes.1118

In summary, large-scale monetary and fiscal stimulus was in play in 2021, primarily due to decisions made early in 2020. This economic stimulus led to an unexpected surge in house prices.

L3.3.6 Opportunities to revisit and improve on decisions were taken but many were missed

I whai wāhi anō ki te arotake me te whakapai ake i ngā whakatau, engari he maha kāore i whāia

The period from February to August 2021 was relatively calm in New Zealand. Decision-makers were not under as much pressure to make frequent quick decisions as they were earlier, and later, in the pandemic. Advisors had more time to reflect on and review decisions taken at speed earlier in the pandemic, and to look for what might be coming over the horizon.

L3.3.6.1 Fiscal policies set in place in 2020 received limited review and adjustment

He iti noa te arotake me te whakatikatika i ngā kaupapa here ā-tahua i whakatūria i te tau 2020

Income support was put in place quickly in 2020. As we have described, the Wage Subsidy Scheme had distinct advantages. The money could be dispensed quickly and once workers were back to work, the payments ceased. However, the opportunity to consider alternatives to the Scheme was not taken.

While the Wage Subsidy Scheme was like the JobKeeper scheme in Australia, other countries took different approaches and spent different amounts on providing income support (Box 6).

| Box 6: Three broad approaches to supporting workers and firms | ||

|---|---|---|

|

Most developed countries offered large-scale economic support for firms and citizens during the pandemic, although the nature and scale of that support varied considerably. Broadly, governments could:

The three approaches have different strengths and weaknesses. 1. Unemployment benefits are designed to soften the blow of an economic downturn for those who lose their jobs as a result. Such benefits have been in existence in New Zealand in some form or other for almost a century.1119 Unemployment benefits have the advantage that the required administrative machinery is already in place, and no active policy or design decisions are required (thus they are often called 'automatic stabilisers'). However, unemployment benefits help protect household incomes – they do not protect jobs or businesses. Involuntary job loss can cause income scarring and loss of human capital.1120 2. Direct payments and tax concessions to businesses can give employers and workers greater confidence that businesses and jobs will survive. If conditional on employment being maintained, they can also preserve the connection between employers and workers, minimising the risk of widespread unemployment in response to an economic shock. They can come at a considerable fiscal cost to the government, but that can be reduced by targeting eligible firms and employees. However, they 'prop up' firms that are otherwise poorly performing. 3. Governments can take an equity stake in firms or make loans and guarantees to firms. These measures may provide less overall confidence to firms than direct payments. However, they may ultimately be cheaper for governments, in that equity stakes can be sold, loans repaid, and not all guarantees will be needed. Different countries took different approaches

|

||

New Zealand's Wage Subsidy Scheme was one of the more expensive responses (as a percentage of GDP).1122

According to a 2023 evaluation by the consulting firm MartinJenkins, officials began exploring options to replace or revise the Wage Subsidy Scheme during the latter part of 2020. Ultimately, the focus turned to 'refining the approach in a shifting context rather than re-examining the settings or revisiting the choice of scheme.'1123 The Wage Subsidy Scheme was essentially unchanged when the Auckland lockdown started in August 2021.1124 However, refinements were made to eligibility criteria, and the amount and frequency of payments, and some of these will have reduced its fiscal cost.1125

The Office of the Auditor-General reported in May 2021 that a 'full and timely' evaluation of the Wage Subsidy Scheme was needed.1126 Later in 2021, the Office reported that progress had been made on planning and organising such an evaluation, with expected completion in the second half of 2022.1127 The evaluation was published in three parts during 2023. However, by this time the pandemic had receded.1128

There are complex trade-offs when designing income support policies and many factors to consider, including whether alternatives can be implemented through existing mechanisms. The Wage Subsidy Scheme was able to be implemented quickly in 2020, but alternatives could have been considered in the event of further lockdowns.

We are not aware of any sizeable component of the fiscal stimulus programme that was reviewed or cancelled to lessen the stimulus once the undesirability of further stimulus became clear. The Shovel-Ready Programme (Box 5), for example, continued as planned.

By August 2021, the Treasury advised shifting towards more targeted fiscal support and recommended against further stimulus from Budget 2022 onwards.1129

L3.3.6.2 Monetary policies adopted in 2020 were generally reviewed and adjusted over time

I te nuinga, i arotakengia, i whakatikatikahia hoki ngā kaupapa here ā-moni i whakaaetia i te tau 2020 i te roanga o te wā

The Monetary Policy Committee meets seven or more times a year. We observed a changing policy stance in the Committee's successive media statements during 2021 and 2022. In February 2021, its statement was titled 'Prolonged Monetary Stimulus Necessary'. This stance remained in the April and May statements, but the July statement expressed inflation concerns:

The Committee agreed that, in the absence of any further significant economic shocks, more persistent consumer price inflation pressure is expected to build over time due to rising domestic capacity pressures and growing labour shortages.1130

The Official Cash Rate was left 'on hold' at 0.25 percent in August, but, consistent with the statement's title 'Monetary Stimulus Reduced', bond purchases under the Large Scale Asset Purchase programme ceased, with total purchases to that date of $53 billion (well short of the $100 billion limit agreed in August 2020).1131

In October 2021 the Monetary Policy Committee raised the Official Cash Rate to 0.5 percent. Its assessment was that:

rising demand alongside capacity constraints is contributing to higher domestic inflation. Cost pressure in New Zealand … is expected to result in CPI inflation rising above 4 percent in the near term, before returning towards the 2 percent midpoint of the target band over the medium term.1132

Over the following 19 months, the Monetary Policy Committee raised the Official Cash Rate in steps to a peak of 5.5 percent in May 2023.1133 It did so to dampen inflation, which peaked at an annual rate of 7.3 percent in June 2022, as measured by changes in the Consumers Price Index.1134

The Monetary Policy Committee process – which involved regularly scheduled reviews, and published decisions and current thinking about future decisions – served New Zealand well in the pandemic.

However, the Reserve Bank's Funding for Lending programme ran to the full length of its pre-committed two-year term, which was to December 2022. This was well beyond the point when, by the Monetary Policy Committee's assessment, monetary stimulus was still needed. The Reserve Bank has recognised that, looking back, it would have been preferable if the programme had been designed with more flexibility, enabling earlier phasing out or termination once the need for monetary stimulus began to lessen.1135

L3.3.7 Monetary and fiscal policies became unaligned from mid-2021

Mai i waenga-tau 2021, kāore i hāngai tahi ngā kaupapa here ā-moni me ngā kaupapa here ā-tahua

From July 2021, the Reserve Bank started winding back its monetary stimulus in response to signs of inflation. The Monetary Policy Statement in August 2021 states:

Members noted that they now had more confidence that rising capacity pressures will feed through into inflation, and that employment is at its maximum sustainable level. Members concluded that they could continue removing monetary stimulus, following their decision to halt additional purchases of government bonds under the LSAP programme at their July meeting.1136

Yet, following the Delta outbreak in August 2021 (which prompted the Auckland lockdown between August and December) government spending increased via the Wage Subsidy Scheme and other business support schemes. Other pre-committed spending was also having a large stimulatory impact.

The Reserve Bank's Chief Economist confirmed in 2025 that, at points in the response, monetary and fiscal policy were pushing in different directions:

The lag and persistence in pandemic-related fiscal spending resulted in fiscal policy continuing to add economic stimulus while monetary policy became restrictive to reduce inflation and keep medium-term inflation expectations in check … In other words, containing inflation over this period required the [Official Cash Rate] to be higher than otherwise if fiscal support during the pandemic had been more timely and temporary.1137

And the Treasury Secretary, in a 2024 speech, noted that 'our assessment is that fiscal policy has contributed to interest rates being higher than otherwise. It [was] not the main driver, but it is a factor among many others.1138

Fiscal and monetary policies became unaligned in 2021. The lag and persistence of fiscal stimulus meant that monetary policy had to work harder to fight inflation.

L3.3.8 Economic forecasts during the pandemic were unreliable

Kāore I te pūmau ngā matapae ōhanga i te wā o te mate urutā

Governments rely on macroeconomic forecasts to inform economic policy. We observed in section 2.4.12 of Part 2 of this report that macroeconomic forecasting did not perform well in the extraordinary circumstances of the pandemic. This was not confined to New Zealand – it was challenging for many countries.1139

Macroeconomic models, which are a major input into forecasts, are mathematically complex. They are largely trained on data covering normal business cycles, which may include some small shocks. But they incorporate limited (if any) data from large economic shocks, and their reliability falls dramatically under those conditions.

The New Zealand Government relies on forecasts to inform whether planned revenue and expenditure will meet the criteria set out in the Public Finance Act 1989. Such questions are at their most pertinent during economic shocks, yet this is when forecasts become much less reliable.

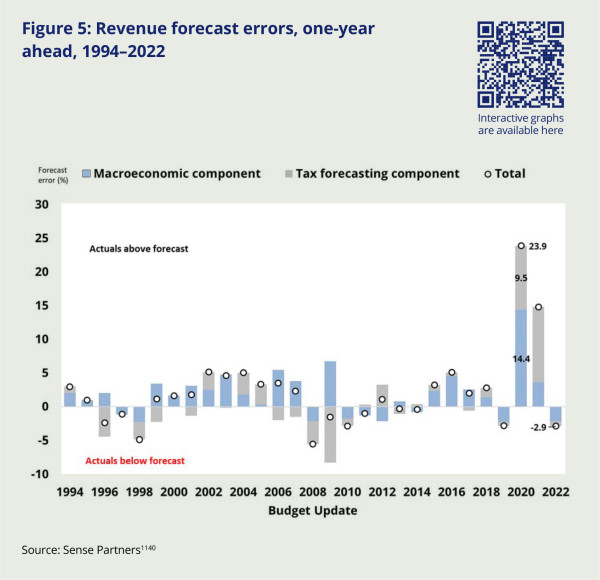

Figure 5 shows the accuracy of the Treasury's revenue forecasts, looking back at them a year later. It highlights the particularly large forecasting errors in 2020 and 2021.

Figure 5: Revenue forecast errors, one-year ahead, 1994–2022

The Reserve Bank has also identified forecasting challenges during the pandemic, writing in 2025:

The Reserve Bank's forecast errors increased significantly during the COVID-19 period between February 2020 and August 2022, primarily due to large and unusual shocks. Large forecast errors were also experienced by private forecasters and other central banks during that period. Since November 2022, our forecasting performance has improved to near pre-COVID-19 levels.1141

L3.3.9 Public debt increased during the pandemic

I piki ake te nama tūmatanui i te wā o te mate urutā

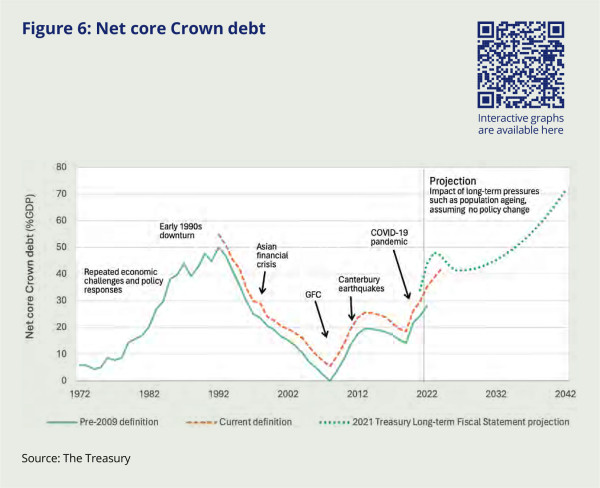

Increased spending and reduced tax revenue combined to sharply increase public debt during and since the pandemic (Figure 6).1142

Figure 6: Net core Crown debt

New Zealand's public debt is not high when compared to other high-income countries.1143 However, the country's natural hazard risk profile is unusually high. As Lloyd's of London reported in 2018, New Zealand has the second highest annual expected losses in the world from natural catastrophes.1144 For example, Treasury has estimated that the fiscal cost of the Canterbury earthquakes was equivalent to 11.3 percent of GDP. It is therefore prudent for New Zealand to ensure the government has the capacity to provide fiscal buffers for large and expensive future events, including pandemics.

The Public Finance Act 1989 is designed to discipline government spending and revenue collection. It includes principles of responsible fiscal management, with section 26G requiring government to:

- reduce total debt to prudent levels and maintain it at those levels

- ensure that on average, over a reasonable period of time, total operating expenses do not exceed total operating revenue

- maintain levels of total net worth that provide a buffer against factors that may impact adversely on total net worth in the future

- manage prudently the fiscal risks facing the government.1145

Section 26G(2) allows the government to temporarily depart from those principles if it explains how and when it will return to them.

The Government used this departure provision during the pandemic, but doing so had consequences. As the Treasury noted in 2025, 'this increasing use of fiscal support has contributed to public debt ratcheting up over time. If nothing changes, this leaves future generations with less financial capacity to respond to shocks.1146 New Zealand now faces difficult challenges in reining in public debt, Treasury stated:

…under current policy settings, New Zealand's fiscal trajectory is not sustainable. Even in favourable scenarios, debt continues to rise. We are currently running a structural deficit, and the buffers that once protected us are eroding.1147

The principles of responsible fiscal management in the Public Finance Act 1989 are sound, including in their provision for crises. Yet increased spending and reduced tax revenue combined to sharply increase public debt during and since the pandemic. This has left New Zealand with less flexibility to respond to shocks, including a future pandemic.

L3.4 What we think is needed

Ā mātou whakaaro mō ngā mea e hiahiatia ana

New Zealand acted swiftly in early 2020, and with considerable effect. Our unicameral Parliament and strong Executive allowed for fast, coordinated action to a rapidly developing shock. Generous support for workers and businesses worked alongside public health measures. Together, they gave people confidence that they would still receive income if they stayed at home and still have jobs and businesses to return to when COVID-19 restrictions lifted.

In this section, we identify economic lessons arising from the pandemic, including an improved understanding of the relevant economic tools and institutions, and how these might be better applied in a future pandemic.

L3.4.1 Avoid irreversible actions and keep future options open

Me karo i ngā mahi kāore e taea te whakahoki, ā, kia tuwhera tonu ngā kōwhiringa mō anamata

In a period of high uncertainty, such as at the start of a pandemic, decisive short-term measures may be needed to reassure the community and maintain economic confidence. But it is important that those short-term measures do not become long-term measures.

In hindsight, some important economic decisions, especially those concerning the use and extent of stimulatory monetary and fiscal policy, were implemented without provision for their reversal (such as the Shovel-Ready Programme) or timely exit (the Funding for Lending programme). Exceptions were policies that switched on and off automatically with alert

level changes (such as the Wage Subsidy Scheme) and programmes that allowed discretion up to an overall funding limit (such as the Large Scale Asset Purchase programme).

The option to change course is important because, in a crisis where there is considerable uncertainty, later information may challenge the original assumptions and understandings that underpinned early decisions. The shift in understanding about the nature of the economic shock caused by COVID-19 is a good example of a circumstance in which the opportunity to reverse earlier fiscal commitments could have been valuable.

It is impossible to know for certain what the exact nature of a future pandemic, or other such shock, will be. So, decision-makers in a future pandemic should retain the option to change course in response to updated information.

L3.4.2 Revisit and evaluate decisions made swiftly in emergency conditions

Arotake anō, ā, aromatawai i ngā whakatau i mahia wawe i raro i ngā āhuatanga ohotata

Moving fast in an emergency has advantages. But, when decisions are taken swiftly, it is unlikely that all available options will be canvassed. For example, the Wage Subsidy Scheme was designed and implemented in a few weeks, and did the job well for the 2020 national lockdown. But it was the single most expensive component of the Government's response to the pandemic. The Scheme could have been reviewed after the 2020 lockdown, and potentially less expensive alternatives fully considered before the extended 2021 lockdowns (see section 3.3.6.1 above).

In a long-running shock such as a pandemic, not all decisions need be taken swiftly – a point we emphasise in Lesson One. Those that are should be reviewed as opportunities arise. Normal standards of policy design and scrutiny should be applied in these reviews.

L3.4.3 Treat macroeconomic forecasts with caution

Me tūpato ki ngā matapae ōhanga whānui

As we have explained, the reliability of the macroeconomic models governments use in economic forecasting falls dramatically during large shocks. In common with many other jurisdictions, forecast errors were unusually large in New Zealand during the pandemic (see section L3.3.8).

When macroeconomic forecasts are suspected to be unreliable, decisionmakers should avoid anchoring on a single predicted path for the economy. A better approach is to develop a range of plausible scenarios to guide policy choices. Scenarios allow consideration of different paths the economy could follow, helping to identify policies that are effective in multiple states of the world.

L3.4.4 Create and maintain systems to gather information and monitor effects of decisions

Waihanga, ā, pupuri hoki i ngā pūnaha hei kohikohi pārongo, hei aroturuki i ngā pānga o ngā whakatau

Lesson One makes the point that some pandemic response decisions were made without sufficient attention to the monitoring required – specifically, what monitoring would be needed to remain confident that the option chosen was achieving its intended purpose, no better option had become available, and no unforeseen consequences had emerged.

This also applies to economic policy: for example, house price inflation in 2020 and 2021 was a largely unforeseen consequence of the monetary and fiscal stimulus policies adopted in March 2020 (see section L3.3.5 above).

Monitoring provides the information required to adjust or refine prior decisions; it needs to be backed by systems and processes that bring that information to the attention of decision-makers, allowing them to adjust policies to reflect the new information.

Good economic policy is based on reliable and timely economic data, and data can change quickly during an economic shock. For example, Consumers Price Index (CPI) data was produced on a 3-month cycle during the pandemic; more frequent data would have helped identify the rampup of CPI inflation in the second quarter of 2021. We acknowledge the

Government’s announcement that monthly CPI will be available from 2027,1148 and also the greater use being made by the Reserve Bank of unofficial, but more timely, economic indicators.1149 We think that more frequent releases of a wide range of macroeconomic indicators could be valuable in future pandemics, and more generally.

L3.4.5 Prepare decision-making principles for those facing an imminent pandemic

Whakarite i ngā mātāpono whakatau mā te

hunga e tū atu ana ki tētahi mate urutā tata

The decision-makers faced with the next global pandemic may have no personal experience of responding to COVID-19. They will benefit from advice that is sufficiently general to be useful, not so generic as to be useless – and, most importantly, short enough to be quickly assimilated and applied.

Box 7 could form the starting point for a short-form guide.

| Box 7: Decision-making principles for those facing an imminent pandemic | ||

|---|---|---|

|

In the early ('acute') stages of a pandemic, decision-makers face deep uncertainty: outcomes and probabilities are unknown, data are incomplete, and inaction (or 'wait and see') can be politically or socially untenable. This applies as much to economic decisions as it does to public health ones. Decisions made under such emergency conditions may prove sub-optimal in hindsight. A useful rule is to avoid policies that cannot be reversed if circumstances change. More generally, in emergency conditions or in the acute phase of a pandemic, decision-makers should aim to:

A broader goal of emergency decision-making is to take actions that accelerate the move back to a more normal world – the 'chronic' phase can be a period in which decisions can be made more slowly and deliberately, drawing on a wider range of expertise, tools and safeguards. In the chronic phase, decision-makers should:

Importantly, persisting with 'emergency' decision-making is undesirable during the extended chronic phase. It will likely lead to burnout and poorer decision-making. |

||

L3.4.6 Maintain rather than build new infrastructure for fiscal stimulus

Pupuri kē i ngā hanganga o nāianei, kaua ngā hanganga hou hei whakaohooho ā-tahua

Should a government choose to provide fiscal stimulus in the event of a pandemic, it will need to decide what parts of the economy it wants to stimulate, and over what timeframe.

Infrastructure projects are often the fiscal stimulus of choice for governments. According to the International Monetary Fund:

As part of stimulus packages, governments often hope to rely on 'shovel-ready' projects that can be kick-started within a few months. Yet countries may find they have few such projects and thus may not be able to increase public investment in time …1150

At the outset of the pandemic, the Treasury and the Ministry of Business, Innovation and Employment advised that spending should be 'timely, temporary and targeted'. Yet infrastructure projects are typically slow to ramp up, with most of the spending likely occurring after the immediate need for fiscal stimulus has passed. It is also hard for governments to abandon promised infrastructure projects, and there may be significant sunk costs if they are curtailed. Moreover, the availability of suitable ('shovel-ready') projects may not be in the places or economic sectors in which the stimulus is needed.

Infrastructure projects are also generally notorious for cost overruns1151 and carry the risk of benefit shortfalls.1152 Value-for-money assessments done quickly (including for projects to qualify as being 'shovel ready') can be wildly incorrect, creating a risk that large amounts of public money will be wasted.1153

Cost overruns generate additional fiscal stimulus. For example, on 31 May 2021, Cabinet approved additional funding for the New Zealand Upgrade Programme of $1.9 billion due to cost overruns. In June 2022, the Treasury identified further cost escalation of $695 million.

By contrast, projects that catch up on deferred infrastructure maintenance or accelerate maintenance programmes do not generally suffer from these problems.1154 Maintenance programmes are also easier to slow down or pause once the need for fiscal stimulus subsides.

According to the New Zealand Infrastructure Commission, around 60 percent of investment needs to go to renewing existing assets, not building more.1155 That suggests that if fiscal stimulus is considered necessary in a future pandemic, maintenance and renewal should be considered ahead of new infrastructure investment.

We think it would be worthwhile to investigate the feasibility of an Infrastructure Maintenance Priorities Programme, modelled on the existing Infrastructure Priorities Programme.1156 The new programme would be an independent and standardised process to identify maintenance proposals and projects for publicly-owned infrastructure across New Zealand that represent good value for money and can be delivered quickly should fiscal stimulus be required.

The Infrastructure Maintenance Priorities Programme's purpose would be to offer central government a screened and pre-approved list of maintenance projects suitable for fiscal stimulus, making it more likely that stimulus spending would be timely, temporary, targeted, and value for money.

The investigation should undertake a full cost-benefit appraisal of such an approach and consider ways to mitigate potential moral hazard issues (such as owners deferring maintenance of their own Infrastructure Maintenance Priorities Programme-listed assets, trusting that central government will fund that maintenance in the next economic downturn).

L3.4.7 Rebuild fiscal buffers to deal with a range of eventualities

Whakarite anō i ngā pūtea ā-tahua hei tauārai i ngā āhuatanga ka pā mai

Governments cannot know when the next pandemic will occur, how long it will last, how expensive it will be and what resources will be required to ameliorate its effects. Nor can a government know when the next pandemic will occur in relation to other economic shocks, including those arising from natural disasters or international events.

In the face of such uncertainty, the best way to prepare for a pandemic is to have fiscal buffers that are capable of dealing with economic shocks, can be drawn on quickly and applied flexibly to deal with a range of eventualities.

The Treasury should regularly report on the country's fiscal resilience. These reports should advise on current and expected public debt levels, whether those levels provide a sufficient fiscal buffer in the face of one or more adverse events comparable in fiscal cost to the COVID-19 pandemic, and on the costs and benefits of maintaining that buffer.

New Zealand's public debt is not high when compared to other high-income countries, but its natural hazard risk profile is unusually high (see section 3.3.9). The country's current level of public debt means that it is in a weaker position to weather the next large economic shock than it was at the start of the COVID-19 pandemic.

Broadly speaking, some combination of three elements is needed to reduce public debt relative to GDP:

- primary fiscal surpluses (which occur when tax revenue exceeds primary government spending)1157

- economic growth at a rate that exceeds the interest rate on the debt1158 and

- inflation.1159

The most palatable option for debt burden reduction is economic growth, driven by productivity improvements1160 and accompanied by fiscal restraint.1161 This option also shares the cost of debt reduction more evenly across generations.

The Public Finance Act 1989 requires the Minister of Finance to present a report on the Government's fiscal strategy on Budget Day. The Fiscal Strategy Report 2025 outlines the Government's intentions to 'put net core Crown debt as a percentage of GDP on a downward trajectory towards 40 per cent' over the next four years, and specifies an objective for the next 15 years: 'Once net core Crown debt is below 40 per cent of GDP, maintain it within a range of 20 per cent to 40 per cent of GDP, subject to economic shocks.1162

The objectives in the Government's annual Fiscal Strategy reports should be assessed against a range of adverse economic scenarios, including one or more COVID-19-sized economic shocks.

L3.4.8 A strong economy will help New Zealand prepare for and respond to a future pandemic

Mā te ōhanga pakari e āwhina a Aotearoa ki te whakarite me te whakautu ki tētahi mate urutā ā muri ake

In terms of health outcomes, New Zealand's experience of the COVID-19 pandemic was very favourable compared with most countries, with very low excess mortality (the increase in the overall death rate over the normal rate). Recent research has compared the age-standardised excess mortality across 193 countries.1163 The differences were stark. The authors identified four criteria associated with low excess mortality: island jurisdictions,1164 high incomes, a favourable location (namely southeast Asia, east Asia, or Oceania) and the adoption of an exclusion/elimination strategy.

- New Zealand met all four of those criteria. Importantly, it appears that a country's opportunity to adopt an exclusion/elimination policy is largely contingent on the other three criteria. While two of those are geographic, the third – being a high-income nation – depends on the medium- to long-term performance of the economy; that is, on New Zealand's ability to efficiently produce the goods and services demanded in global markets, supported by prudent economic policies.

New Zealand's economic policy decisions now and into the future will be important for determining the country's ability to mount a strong response to the next pandemic or other such shock.

L3.4.9 Seek a better understanding of unconventional monetary policies

Kimihia te mārama hōhonu ake ki ngā kaupapa here ā-moni kāore i te tikanga

Unconventional monetary policies – which, in New Zealand's response, took the form of the Large Scale Asset Purchase and Funding for Lending programmes – were widely used during the pandemic. The short- and longrun effects of these policies are subject to ongoing debate. At the present time it would be difficult to either rule out or endorse their future use.

We do know that programmes that attempt to shift long-term interest rates, such as the Large-Scale Asset Purchase programme, can be very expensive. They are trying to push interest rates to levels that the market does not want them at, and it requires money to achieve that aim.

Current estimates put the losses from the Large-Scale Asset Purchase programme at $10.5 billion. The Reserve Bank has recently argued that these fiscal losses have been offset by other fiscal and wider economic benefits.1165 By contrast, a former member of the Bank of England's Monetary Policy Committee has argued that the effects on interest rates of quantitative easing in the UK were likely to have been 'small and temporary'.1166

Even if the Reserve Bank's assessment is correct, it will not necessarily be the case for quantitative easing applied in future pandemics, particularly if the Official Cash Rate is not near the effective lower bound going into the pandemic.

Further, the Reserve Bank's assessment does not answer the question of whether that $10.5 billion could have been better spent, nor whether the outcome desired could have been achieved at a lower cost to New Zealand.

Similar questions surround the use of forward guidance and the Funding for Lending programme.

There remains significant uncertainty about the unconventional monetary policies used during the pandemic. They should be subject to further rigorous empirical and policy analysis between now and the next economic shock.

L3.4.10 Be clear about the roles of fiscal and monetary policy during a pandemic

Kia mārama te wehewehe i ngā tūranga o te kaupapa here ā-tahua me te kaupapa here ā-moni i te wā o te mate urutā

As we have seen, both fiscal and monetary policy can shift demand for goods and services, constrained by the potential output of the economy.

In New Zealand and overseas, the established assignment of roles – the so-called 'consensus assignment' – is for fiscal policy to be focused on the effective management of public resources and finances, on a medium- to long-term basis; leaving macroeconomic stabilisation to monetary policy.1167

In New Zealand, fiscal policy extended beyond responding to the pandemic itself, taking on a sizeable and active macroeconomic stabilisation role by funding projects and programmes for the purpose of providing additional stimulus. Meanwhile monetary policy also expanded its role, through the development and implementation of the unconventional monetary policies just described. Overall, these responses could be characterised as ‘all hands on deck’.1168

Phase One of this Inquiry concluded that there was no active coordination of monetary and fiscal policy in the economic response to the pandemic, in the sense of having a broad common understanding of how they might interact with each other.1169

Building on that analysis, we make a distinction between coordination and alignment. Coordination is between institutions, in this case between the Minister of Finance (advised by the Treasury) and the Reserve Bank. It is about sharing data, thinking and intentions, and joint efforts to resolve uncertainties. Alignment is about policies – whether they pull in the same direction, or against each other.

Phase One saw no evidence of the Reserve Bank and the Treasury jointly advising the Government in a coordinated manner on the broad pattern of how the quantum and mix of fiscal and monetary stimulus should be provided, or on how the quantum and mix of stimulus should be adjusted as the pandemic evolved. We observed that monetary and fiscal policies became unaligned – working against each other – in 2021 (section 3.3.7).1170

The Reserve Bank, which is responsible for monetary policy, is operationally independent from the Government, which is responsible for fiscal policy. The benefits of Reserve Bank independence outweigh its potential drawbacks.

But before the next pandemic, we think it would be helpful if the Reserve Bank and the Government developed a shared high-level view of the respective roles of fiscal policy and monetary policy in responding to large economic shocks such as those caused by pandemics, based on the comparative advantage of each institution.

The Treasury's 2025 long-term insights briefing has set out a view, with which we concur.1171 However, we consider it leaves room for more clarification of the respective roles of fiscal and monetary policies when monetary policy is constrained by the effective lower bound.

L3.4.11 Improve the process and increase transparency of Crown indemnities

Whakapai ake i te tukanga, ā, whakanui i te mārama o ngā taunahatanga Karauna

Guarantees and indemnities are contingent liabilities that can expose the Crown to significant future fiscal costs (see section 3.3.4.3).

The Public Finance Act 1989 provides for the Minister of Finance to issue Crown guarantees and indemnities. The only condition is that ‘it appears to the Minister to be necessary or expedient in the public interest to do so’.1172 ‘Necessary’, ‘expedient’ and ‘public interest’ are not defined.1173 Transparency requirements – presenting a statement to the House of Representatives – apply to liabilities of $10 million or more. Further, the Act does not require the government to keep an up-to-date list of its cumulative contingent liabilities resulting from Crown guarantees and indemnities.1174

The evaluation process, and transparency and accounting requirements, appear underpowered for risks to the Crown that could potentially amount to billions of dollars. A future government faced with a pandemic might also need to consider issuing large indemnities, so it is appropriate to match the level of scrutiny to the size of contingent liabilities.

L3.5 Recommendations | Ngā tūtohutanga

Recommendation 3A:

Prepare guidance for decision-makers in a future pandemic

The 'strategic function' recommended in Lesson One should prepare and maintain a short-form guide for decision-makers facing a pandemic. (See Recommendation 1D.)

Recommendation 3B:

Advice on prudent debt levels in the face of future shocks

At least once every four years, the Treasury should publish a Financial Resilience report on the country’s fiscal resilience. In the report, the Treasury should advise on current and expected public debt levels, whether those levels provide a sufficient fiscal buffer in the face of one or more adverse events comparable in fiscal cost to the COVID-19 pandemic, and on the costs and benefits of maintaining that buffer. (This builds on Recommendation 25f in the Phase One report.)

Recommendation 3C:

Outline plans to rebuild fiscal buffers

The Government should assess the objectives stated in its annual Fiscal Strategy reports in light of the Treasury's most recent Financial Resilience report. (See Recommendation 3B above.)

Recommendation 3D:

Improve coordination between fiscal and monetary institutions

The Government, advised by the Treasury and the Reserve Bank, should clarify the roles of fiscal and monetary policies in the event of a large economic shock of uncertain nature and duration. (This builds on Phase One Recommendations 25a–d.)

Recommendation 3E:

Develop options for implementable income and business support before the next pandemic

The Treasury, in conjunction with relevant agencies, should develop policy options for financial assistance schemes during a pandemic.

Recommendation 3F:

Increase the frequency of official economic statistics

Stats NZ, in consultation with the Treasury and the Reserve Bank, should investigate the costs and benefits of more frequent releases of a wide range of macroeconomic indicators.

Recommendation 3G:

Investigate the feasibility of an infrastructure maintenance priorities programme

The Treasury, in collaboration with the New Zealand Infrastructure Commission, should investigate the feasibility of an Infrastructure Maintenance Priorities Programme for publicly owned infrastructure, with the aim of making it more likely that future fiscal stimulus would be timely, temporary and targeted, and value for money. (This builds on Recommendation 25g in the Phase One report.)

Recommendation 3H:

Seek a better understanding of unconventional monetary policies

The Treasury and the Reserve Bank should initiate a research programme to subject the unconventional monetary policies used in New Zealand and other countries during the pandemic to further rigorous empirical and policy analysis.

Recommendation 3I:

Improve the process for, and increase transparency of, Crown indemnities

The Government should review the sections of the Public Finance Act 1989 that deal with giving Crown guarantees and indemnities. The Act should specify more robust and transparent processes for giving large guarantees and indemnities.

1066 NZ Royal Commission of Inquiry into COVID-19 Lessons Learned: Phase Two (2026), Pandemic Perspectives, https://www.covid19lessons.royalcommission.nz/reports-lessons-learned/phase-two/pandemic-perspectives, pp 83–87

1067 NZ Royal Commission of Inquiry into COVID-19 Lessons Learned: Phase Two (2026), COVID-19 by the Numbers, https://www.covid19lessons.royalcommission.nz/reports-lessons-learned/phase-two/covid-19-by-the-numbers/

1068 The Commission met with Dr Alan Bollard, Dr Graham Scott, Dr John McDermott and Dr Arthur Grimes on 29 October 2025. They have held many senior positions in New Zealand and overseas, including Governor (AB), Assistant Governor (JM), Chairman (AG) and Chief Economist (AG, JM) of the Reserve Bank, Treasury Secretary (GS, AB), Professor at New Zealand universities (AG, AB), Chair of the New Zealand Infrastructure Commission (AB), Chair of the Commerce Commission (AB), Commissioner at the New Zealand Productivity Commission (GS), and Executive Director of the Asia-Pacific Economic Cooperation (AB).

1069 Including the former Prime Minister, Minister of Finance and Minister for COVID-19 Response.

1070 The Treasury, Te Ara Mokopuna: Treasury's 2025 Long-term Insights Briefing (August 2025), https://www.treasury.govt.nz/sites/default/files/2025-08/te-ara-mokopuna-ltib-2025.pdf

1071 Reserve Bank of New Zealand, Macroeconomic and fiscal impacts of quantitative easing in New Zealand (October 2025), https://www.rbnz.govt.nz/-/media/project/sites/rbnz/files/publications/analyticalnotes/2025/macroeconomic-and-fiscal-impacts-of-quantitative-easing-in-nz.pdf; Reserve Bank of New Zealand, Simulating the effects of different monetary policy settings after the COVID-19 pandemic using the Reserve Bank's macroeconomic forecasting model (September 2025), https://www.rbnz.govt.nz/-/media/project/sites/rbnz/files/monetary-policy/mini-rafimp/simulating-theeffects-of-different-monetary-policy-settings-after-covid-19.pdf; Reserve Bank of New Zealand, 'Strong progress made on post-COVID-19 recommendations for monetary policy' (29 September 2025), https://www.rbnz.govt.nz/hub/news/2025/09/strong-progress-made-onpost-covid-19-recommendations-for-monetary-policy

1072 The OCR is the interest rate the Reserve Bank of New Zealand charges banks to borrow money from it, and

the rate the Reserve Bank pays banks who deposit money with it.

1073 This paragraph reports changes in seasonally adjusted, quarterly, real, production-based GDP.

1074 Reserve Bank of New Zealand, 'Gross Domestic Product (M5)' (released 18 September 2025), https://www.rbnz.govt.nz/statistics/series/economic-indicators/gross-domestic-product

1075 Between the December 2019 and the December 2021 quarters.

1076 Measured from December 2007 to June 2009.

1077 The Treasury, Te Ara Mokopuna: Treasury's 2025 Long-term Insights Briefing (August 2025), https://www.treasury.govt.nz/sites/default/files/2025-08/te-ara-mokopuna-ltib-2025.pdf

1078 The Treasury, Te Ara Mokopuna: Treasury's 2025 Long-term Insights Briefing (August 2025), https://www.treasury.govt.nz/sites/default/files/2025-08/te-ara-mokopuna-ltib-2025.pdf, p 23

1079 Austan Goolsbee, Chad Syverson, 'Fear, Lockdown, and Diversion: Comparing Drivers of Pandemic Economic Decline 2020,' NBER, Working Paper 27432 (2020), https://doi.org/10.3386/w27432